The successful listing of the new-style tea beverage brand BANDLUCK (Chagee) on the NASDAQ stock market on April 17, 2025, not only marks a potential thaw in Chinese companies' access to the U.S. capital market but also brings the global ambitions of China's vast and highly competitive new-style tea beverage industry into the spotlight.

BANDLUCK's valuation reached $2.1 billion at its listing, creating a new billionaire in its 30-year-old founder, Zhang Junjie, and its exploration of the global expansion of Chinese tea beverages holds positive significance.

The IPO raised $411 million, and BANDLUCK's American Depositary Shares (ADSs) surged 16% on the first trading day, closing at $32.44. This performance stands in stark contrast to the quiet period of large-scale Chinese company IPOs in the U.S. over the past two years. Previously, due to factors such as Sino-U.S. tensions, Chinese companies' listings in the U.S. had nearly frozen.

BANDLUCK's IPO is not just a milestone for one company; it is also a potential indicator that the market is willing to make selective bets on high-quality Chinese consumer brands, provided these brands have healthy unit economics and a clear international growth story, even amid the current complex and volatile geopolitical situation.

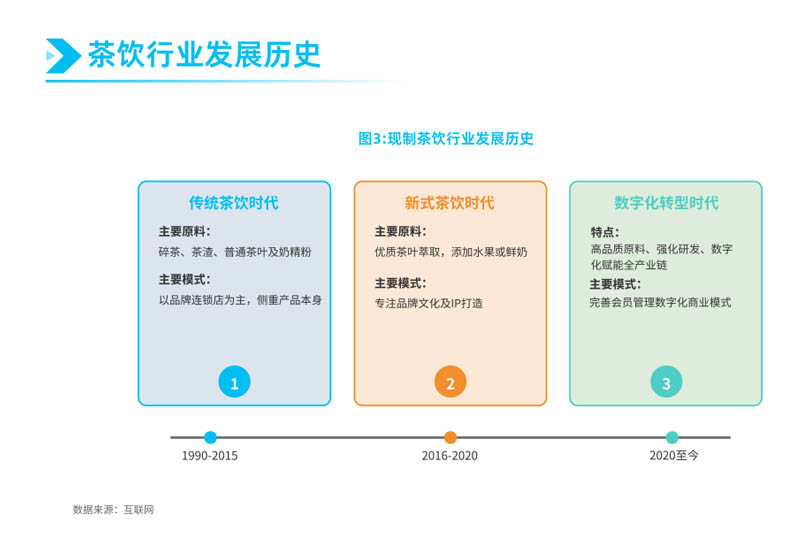

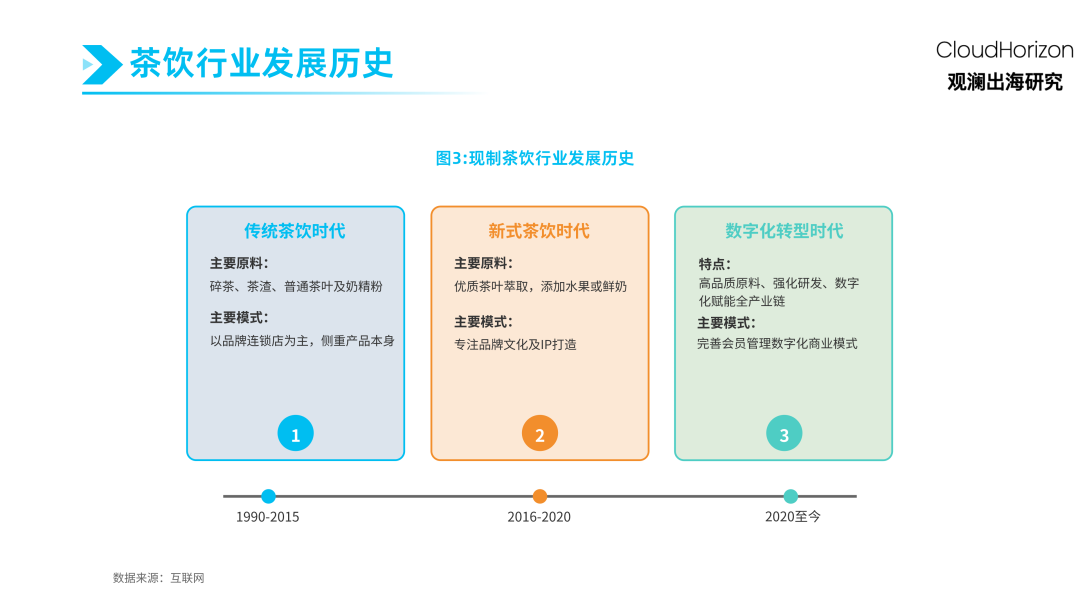

BANDLUCK's international journey stems from its rise in China's fiercely competitive freshly-made beverage market. According to estimates by the China Chain Store & Franchise Association (CCFA), this market has an annual sales volume exceeding 550 billion yuan (approximately $80 billion). China's vast market, rapid product iteration, intense price competition, and ever-changing consumer habits have honed the skills of Chinese tea beverage brands. The gradual saturation of the domestic market and the extremely high store density in first- and second-tier cities have forced brands to penetrate lower-tier markets with relatively lower purchasing power and actively seek growth opportunities outside China. These factors are key drivers accelerating the global expansion of Chinese tea beverage brands. On the other hand, the rapid export of Chinese culture and the acceleration of international cultural exchanges have also facilitated the overseas expansion of tea beverages.

Figure 1: Rapid Development of the Tea Beverage Industry

I. The "Great Voyage" of Tea Beverages: A Surging Wave of Global Expansion

BANDLUCK is just a prominent representative of this wave of globalization among Chinese tea beverage brands. Driven by both domestic market pressures and the higher growth potential and profit margins overseas, these companies are accelerating their global footprint, particularly in Southeast Asia.

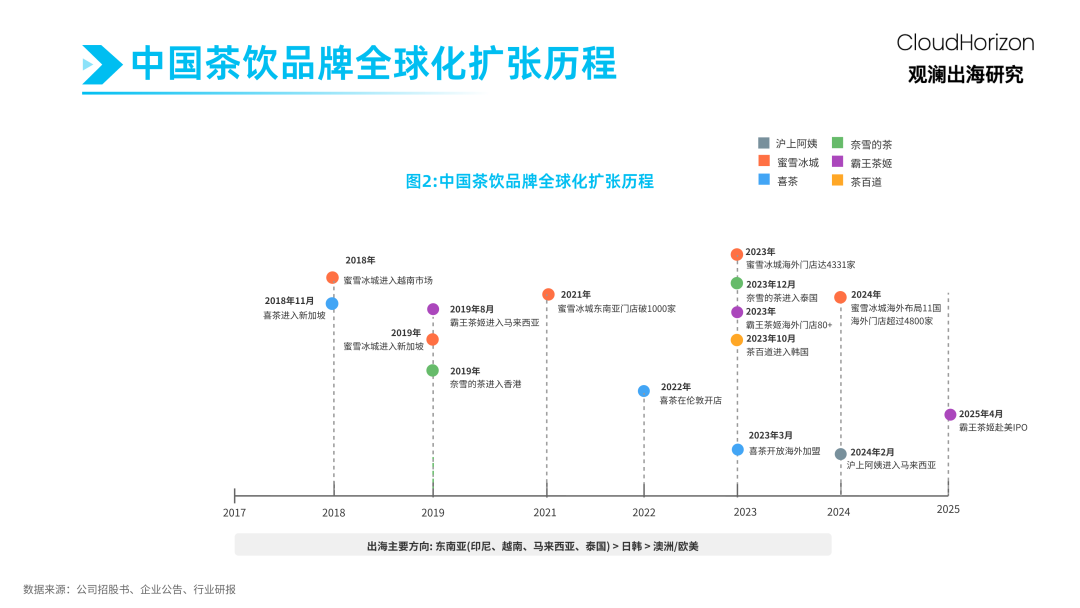

Leading in absolute scale is Mixue Bingcheng. Since opening its first overseas store in Hanoi, Vietnam, in 2018, its international network has exploded. By the end of 2024, it had expanded to 11 countries with a total of over 4,800 overseas stores. Its strategy relies on aggressive franchise expansion and cleverly leverages existing local Chinese business networks (initially utilizing distribution channels of smartphone brands like OPPO and VIVO). Its extremely low price points (typically $1-2 per cup), even with slight increases overseas due to logistics and import costs (e.g., about 1.3-1.4 times the price in China in Indonesia), still pose a significant price challenge to established brands like Starbucks and local chains.

Following Mixue Bingcheng, mid-to-high-end brands are also actively expanding:

* Heytea: Has entered 7 countries including Singapore, the UK, Australia, Canada, and the U.S., focusing on high-traffic urban core locations and targeting consumers familiar with global trends and demanding quality.

* Nayuki: Opened an overseas flagship store in Bangkok, Thailand, showing its intent to compete in the premium market of major capital cities in Southeast Asia.

* BANDLUCK: Beyond the NASDAQ listing providing funding for future expansion, it already has over 150 international stores in Malaysia, Thailand, Singapore, and other locations, adhering to its core "fresh milk tea" positioning and consistent brand image.

* Other Players: Smaller but equally ambitious chains like CoCo, Gongcha, and Guming are also actively expanding their international presence.

Figure 2: The Global Expansion Journey of Tea Beverages

II. Strategic Beachhead: Why Southeast Asia Has Become the "Second Home Market"?

The collective focus of Chinese tea beverage brands on the Southeast Asian (SEA) market is no coincidence. The region combines multiple favorable factors, making it an almost perfect "second home market":

Market Size and Explosive Growth:

According to Mixue Bingcheng data, the freshly-made beverage market in Southeast Asia reached $20.1 billion in 2023 and is projected to surge to $49.5 billion by 2028, with a compound annual growth rate (CAGR) of 19.8%. The freshly-made tea segment is growing even faster, expected to increase from $6.3 billion to $16.6 billion over the same period, with a CAGR of 21.3%. This growth rate far exceeds the global average (about 7.2%) and contrasts sharply with more mature markets.

Demographic Dividend:

Southeast Asia has a notably young population. Countries like Laos (median age 23.5), Cambodia (24.8), the Philippines (25.7), and Indonesia (29.7) have large Gen Z and millennial consumer bases—the core audience for trendy, affordable luxury items like new-style tea beverages. This contrasts with the aging populations in East Asia and some Western countries.

Favorable Operating Environment:

Climate:

Most of Southeast Asia has a tropical climate, meaning cold beverage demand is strong year-round, significantly reducing the seasonal fluctuations common in northern China.

Cost Structure:

Although varying by country, labor and rental costs in many Southeast Asian markets are significantly lower than in China's first-tier cities, potentially improving unit economics, especially for franchise models.

Cultural Affinity:

Shared cultural elements and a historical preference for tea in many Southeast Asian countries may lower the barriers to market entry and consumer acceptance compared to Western markets.

Low Chainization Rate:

The current market is highly fragmented. The chainization rate for freshly-made tea beverages in Southeast Asia is estimated to be less than 10%, compared to about 40% in China. This leaves vast room for Chinese brands with mature chain operation experience and capital strength to leverage their standardization and scale advantages to consolidate the market.

03. Overseas Expansion Strategies: Differentiated Path Choices

The overseas expansion of freshly-made tea beverage brands shows diversified strategic paths, mainly divided into the following models:

(I) Mixue Bingcheng Model: Scale is King, Price Leads

Mixue Bingcheng leads the overseas expansion trend with a model of "extreme cost-effectiveness + franchise-driven + regional intensive layout":

1. Expansion Speed and Scale:

Since opening its first overseas store in Vietnam in 2018, by the end of 2024, the number of overseas stores exceeded 4,800, covering 11 countries and regions, including 2,667 in Indonesia and 1,304 in Vietnam, achieving economies of scale in regional markets.

2. Franchise-Driven Strategy:

Replicated the successful domestic franchise model in Southeast Asia, accelerating expansion through highly attractive terms (e.g., waiving franchise and management fees for two years in Vietnam). Initially leveraged the channel resources of Chinese brands like OPPO and VIVO in Southeast Asia to quickly establish a franchise network.

3. Pricing and Supply Chain Strategy:

Overseas product pricing, though higher than domestic (e.g., about 1.3-1.4 times the domestic price in Indonesia), still maintains a clear price advantage over local competitors. Material supply largely relies on domestic sources, with only perishables procured locally. Plans to build a multi-functional supply chain center in Southeast Asia by 2025, increasing the local procurement share from about 30% to 50%.

(II) BANDLUCK Model: Differentiated Products, Capital Empowerment

BANDLUCK has carved out an overseas path of "focus on fresh milk tea + capital markets + differentiated brand":

Product Differentiation:

Adheres to the core positioning of "fresh leaf milk tea," creating a unique selling point in a market with severe product homogenization. From 2022 to 2024, approximately 79%/87%/91% of BANDLUCK's GMV in China came from its signature fresh leaf milk tea, with about 44%/57%/61% from its top three bestselling fresh leaf milk tea products.

Efficient Operation Model:

Improves store efficiency through a large single-product strategy, using automated equipment to enable staff to make a standard drink in 8 seconds. The top 30% of stores achieve daily sales of over 1,300 cups, laying the foundation for consistent quality control in overseas stores.

Capital Market Empowerment:

Successfully listed on NASDAQ in April 2025, raising $411 million, providing ample funds for global expansion. The prospectus explicitly allocates part of the funds to accelerate international layout, especially supply chain construction in Asian markets.

(III) Premium Brand Model: Boutique Strategy, Urban Core

Premium brands represented by Heytea and Nayuki adopt a strategy of "boutique stores + core business districts + brand upgrade":

Selective Entry:

Heytea has entered 7 countries including Singapore, the UK, Australia, Canada, and the U.S., but with a limited number of stores, adopting a boutique approach.

Core Business District Strategy:

Store locations focus on core business districts and high-end shopping malls, with brand image building as the core. For example, Nayuki chose a well-known commercial complex in Bangkok, Thailand, for its flagship store.

Brand Upgrade and Localization:

Integrate with local cultural elements to launch innovative products that suit local tastes, emphasizing the brand's fashionable and premium positioning to attract quality-conscious consumers.

Figure 3: Overseas Expansion Status of Major Tea Beverage Brands

IV. Future Outlook: Long-Term Potential of Tea Beverage Globalization

(I) Market Expansion Space Forecast

Deep Penetration in Southeast Asia:

Based on population density, major Southeast Asian markets still have huge penetration potential. Taking Mixue Bingcheng as an example, even in its most densely covered markets, Indonesia and Vietnam, store density (0.96/1.30 stores per 100,000 people) is still lower than in its least dense province in China (1.68 stores per 100,000 people). Based on population, just eight Southeast Asian countries have room for over 15,000 additional stores.

Breakthrough in High-End Markets in Europe and America:

As the influence of Chinese tea culture grows, acceptance of high-quality Chinese-style tea beverages in European and American markets is gradually increasing, expected to become the next key expansion area.

Next-Generation Product Innovation:

With the development of the "tea-ification" trend, innovative beverages centered on tea will continue to emerge, potentially replicating the global success path of coffee.

(II) Globalization of the Industry Chain and Cultural Export

Global Tea Industry Chain Integration:

The global expansion of Chinese tea beverage brands will drive the upgrade of the entire industry chain, including tea cultivation, processing, and equipment manufacturing, enhancing China's voice in the global tea industry.

Expanded Cultural Influence:

Through the modern vehicle of freshly-made tea beverages, traditional Chinese tea culture is expected to reach the world in a more accessible way, enhancing China's cultural soft power.

Export of Innovative Models:

The innovative digital operation models, membership systems, and supply chain management experiences of Chinese tea beverage brands will have a profound impact on the global food and beverage retail industry.

V. Conclusion: Chinese Tea Beverages Moving Towards Globalization

The global expansion of Chinese-style tea beverages is in an acceleration phase. This process is not only the expansion of corporate business territories but also the export of Chinese culture and business models. Unlike the globalization of Coca-Cola and Starbucks, which represented the export of American culture and business models, the globalization of Chinese-style tea beverages carries the modern interpretation and innovative diffusion of Chinese tea culture.

As brands like Mixue Bingcheng, BANDLUCK, and Heytea continue to deepen their presence in international markets, Chinese-style tea beverages are expected to become the next truly globally influential beverage category after American-style coffee. In this process, how to balance standardization and localization, and how to address challenges such as supply chain, talent, and cultural adaptation, will determine the speed and depth of the globalization of Chinese-style tea beverages.

With increasing market regulation in Southeast Asia, Chinese tea beverage brands expanding overseas face dual tests of compliance and survival. Whether it's in-depth research on local tea beverage markets, building compliant structures, or recruiting localized talent—key issues in overseas expansion—systematic solutions are needed. Xiaofeilong provides professional full-chain compliance hosting services and localized operational support, helping you build a moat for long-term, stable operation and unlock new growth opportunities in the Southeast Asian tea beverage market. Those who standardize first, land first, will seize the market opportunity ahead.